Explore how the Martingale strategy works in forex and CFD trading, why position doubling creates margin pressure, and how leverage, instruments and risk controls affect outcomes.

Why Is the Martingale Strategy Controversial?

The Martingale strategy has long been controversial in trading because it introduces a seemingly simple logic into highly uncertain markets: increasing position size after a loss and waiting for the next favorable move to cover previous losses. This logic can appear intuitively attractive in a single sample, but under real-world conditions such as consecutive losses, continuing trends, and limited capital, risk can accumulate rapidly.

Historically, Martingale was not originally a financial trading strategy, but a betting system popular in 18th-century France. Later, the concept of martingales in probability theory gradually developed in the 20th century. Paul Lévy used similar conditions in the 1930s, Jean Ville promoted the development of related terminology around 1939, and Joseph L. Doob made important contributions to modern martingale theory. Therefore, in educational writing, a more accurate statement is that the Martingale trading strategy borrows ideas from early betting systems and probability theory concerning fair processes, rather than being a forex trading method directly invented by a single mathematician.

Forex trading, officially known as Foreign Exchange and abbreviated asFX, and contracts for difference, officially known as Contract for Difference and abbreviated asCFD, may both use margin mechanisms. Margin allows traders to control larger notional positions with smaller amounts of capital, which also makes the position-increasing effect of Martingale more pronounced.

From Fair Games to Market Trading

In a fair game, if each outcome is independent and the probability of winning and losing is the same, the probability of success on the next attempt does not automatically increase simply because previous attempts have resulted in losses. In a gambling context, Martingale is often misunderstood as “the more losses occur, the closer the reversal becomes,” but this involves the gambler’s fallacy. Market trading is not exactly the same as coin tossing, because prices are affected by liquidity, interest rates, order books, macroeconomic data, and trader behavior. However, the market also does not necessarily compensate an account in the next trade simply because it has already suffered losses.

Mean reversion does exist in some financial market scenarios. For example, certain currency pairs may repeatedly fluctuate around the midpoint of a range during low-volatility periods, and some carry trades may adjust around long-term valuation centers. However, mean reversion is not a constant rule. Trending markets may last for days, weeks, or even months. Forcing larger positions after losses may exhaust margin before prices revert.

The Mathematical Structure of the Martingale Strategy

Position Increases and Exponential Growth

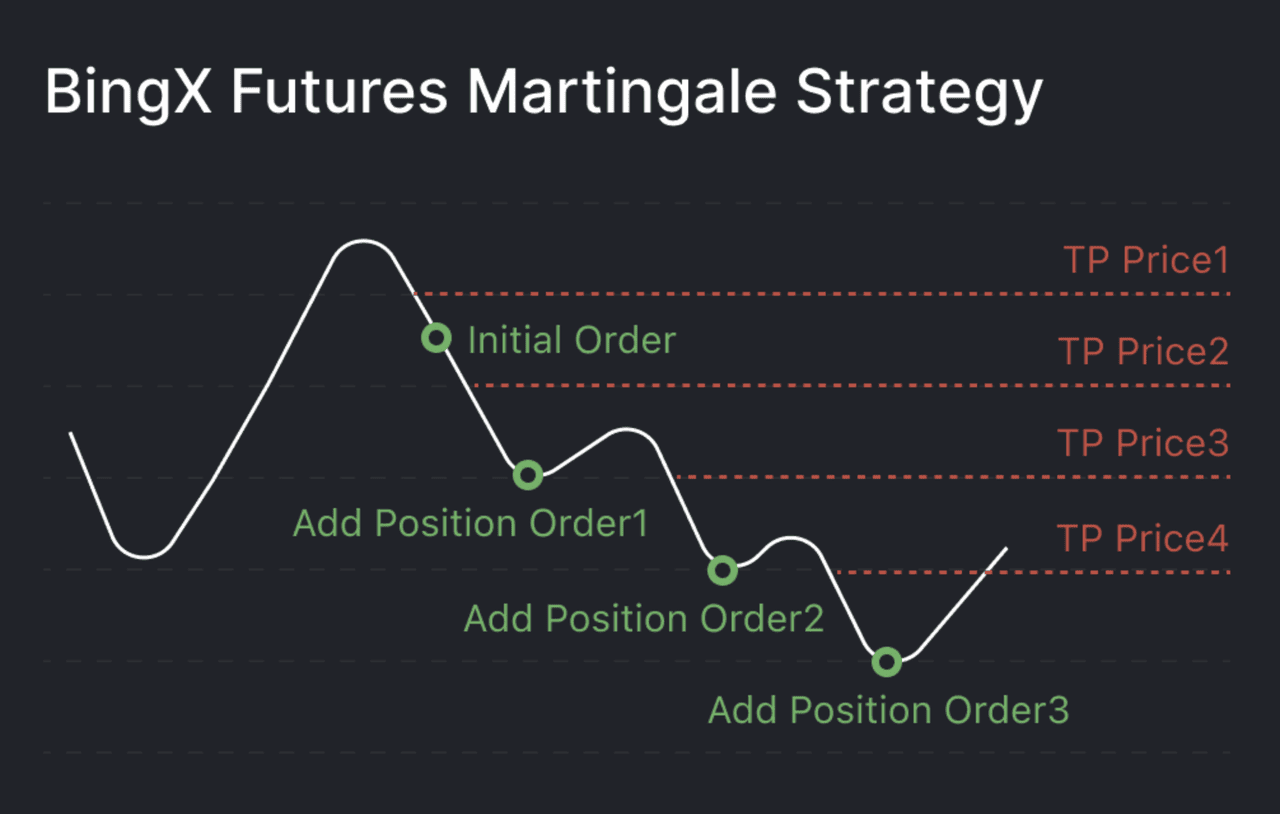

The typical rule of traditional Martingale is to double the next position after a loss. If the initial position is 1 unit, the next positions after consecutive losses will be 2, 4, 8, 16, and 32 units. Cumulative exposure also rises quickly: after 5 losses, the cumulative input is 1 plus 2 plus 4 plus 8 plus 16, or 31 units. If a 6th trade is required, the single position has already reached 32 units.

This shows that the real risk of Martingale is not in the first trade, but in the tail risk after consecutive losses. Tail risk refers to low-frequency but high-impact adverse outcomes. In a trading account, it may appear as consecutive stop-losses, prolonged one-way markets, sudden spread widening, reduced liquidity, or forced liquidation.

| Number of Losses | Key Parameter | Applicable Scenario | Main Risk |

|---|---|---|---|

| 1 loss | The next position is 2 times the initial position | Short-term drawdown observation | Risk begins to exceed the original plan |

| 3 losses | The next position is 8 times the initial position | Stress testing for range-bound models | Cumulative losses have already increased significantly |

| 5 losses | The next position is 32 times the initial position | Extreme scenario analysis | Margin requirements may approach the account limit |

| 7 losses | The next position is 128 times the initial position | Not suitable as a normal live-trading assumption | Most retail accounts would struggle to withstand it |

How Margin and Leverage Change the Outcome

The basic formula for margin trading is: required margin equals notional principal divided by the leverage multiple. If the notional position is USD 100,000 and leverage is 1:100, the initial margin is about USD 1,000. If leverage is 1:500, the initial margin is about USD 200. Leverage lowers the threshold for opening a position, but it does not reduce the profit or loss generated by price movements on the notional position.

Under the EU retail CFD framework, the leverage cap is usually 30:1 for major currency pairs, 20:1 for non-major currency pairs, gold, and major indices, 10:1 for other commodities and non-major indices, 5:1 for stock-based CFDs, and 2:1 for crypto-asset CFDs. Some international accounts may offer higher leverage, such as 1:100, 1:200, or higher, but higher leverage also means a lower margin buffer.

Theoretical Differences Between Martingale Variants

Traditional Martingale and Grand Martingale

Traditional Martingale increases the position by a multiple, while Grand Martingale adds an extra unit after doubling. For example, if the previous trade was 0.10 lot, the next trade after a loss is not 0.20 lot, but 0.21 lot or higher. The purpose is usually to let the next favorable move cover the loss and generate one additional small unit of gain, but it also increases the speed of margin consumption.

Reverse Martingale

Reverse Martingale usually increases position size after a profit and returns to the initial position size after a loss. It is closer to trend-following logic and emphasizes expanding profit potential when a favorable direction continues. Compared with traditional Martingale, it does not continuously increase risk after losses. However, if the position becomes too large near the end of a trend, it may still suffer significant drawdowns.

Pyramiding Method

Pyramiding generally requires new positions to be built on existing unrealized profits, and subsequent positions are usually smaller than or no larger than the previous layer. Its goal is not to cover all losses through a single rebound, but to participate gradually after a trend is confirmed. It has some connection with the idea of following the primary trend inDow Theory, and is also similar to the progressive position-building approach emphasized by trend-following traders in the mid-to-late 20th century.

| Strategy Type | Key Parameter | Applicable Scenario | Main Risk |

|---|---|---|---|

| Traditional Martingale | Doubles after a loss | Short-term mean-reversion assumption | Risk expands rapidly in sustained trending markets |

| Grand Martingale | Adds a fixed unit after doubling | Theoretical model requiring faster loss recovery | More dependent on capital size than the traditional method |

| Reverse Martingale | Adds after profits and reduces back to the initial size after losses | Trend continuation and breakout following | Trend reversals can affect later added positions |

| Pyramiding | Layered participation based on floating profits | Medium-term trends and swing markets | Adding positions too frequently may increase drawdowns |

Differences When Applied Across Instruments

The Martingale strategy is not suitable for applying the same parameters to all instruments. Major currency pairs usually have relatively strong liquidity, but spreads and slippage may still widen around central bank rate decisions, non-farm payroll data, and major political events. Gold and crude oil are affected by macro expectations, inventory data, and safe-haven sentiment, and their short-term volatility may be significantly higher than that of major currency pairs. Index CFDs are affected by constituent stocks, futures markets, and trading hours, making gap risk more prominent. Crypto-asset CFDs have higher volatility, while weekend markets and regulatory news may also bring additional uncertainty.

| Instrument Type | Key Parameter | Applicable Scenario | Main Risk |

|---|---|---|---|

| Major currency pairs | Clear pip value and commonly lower spreads | Range-bound observation and low-frequency testing | Macroeconomic data may cause one-way breakouts |

| Gold and commodities | Larger volatility, with contract specifications requiring verification | Safe-haven themes and commodity cycle research | Rapid volatility increases margin-call pressure |

| Index CFDs | Affected by trading sessions and constituent stocks | Equity market theme observation | Opening gaps may bypass expected execution prices |

| Crypto-asset CFDs | High volatility, with leverage usually more restricted | High-volatility asset research | High risk of consecutive volatility and liquidity gaps |

Why Historical Cases Cannot Directly Prove Strategy Effectiveness

The original text mentions some well-known investors and traders. These cases can illustrate the diversity of capital market approaches, but they cannot directly prove that Martingale is suitable for trading. Value investing, quantitative trading, event-driven strategies, and corporate investment strategies all have independent research frameworks, risk budgets, and investment horizons. When placing them alongside a position system that doubles after losses, it is necessary to avoid implying that all successful trading comes from the same money management method.

For example, long-term investing emphasizes business value, cash flow, and margin of safety; algorithmic trading relies on data, models, execution, and risk monitoring; trend following focuses on price breakouts, volatility, and drawdown control. Martingale mainly deals with position changes after losses and lacks independent directional judgment. Without clear entry rules, a maximum number of layers, total risk limits, and exit rules, it is more like a high-risk capital escalation model.

Martingale Strategy FAQs

What is the core assumption of the Martingale strategy?

Its core assumption is that prices or outcomes will move favorably at some point in the future, and that account capital is sufficient to support previous consecutive losses. In real trading, neither condition can be assumed by default.

Why is the Martingale strategy related to the gambler’s fallacy?

If traders believe that the probability of the next profitable trade must increase after consecutive losses, this is close to the gambler’s fallacy. The outcome of each trade still depends on market conditions, strategy quality, and execution environment, rather than the number of previous losses itself.

Do EU retail CFD leverage limits affect Martingale?

Yes. Lower leverage means more margin is required for the same notional position, reducing the number of position-increase layers an account can withstand. However, higher leverage does not mean lower risk; it only lowers the threshold for opening a position.

Is Reverse Martingale more robust than traditional Martingale?

Reverse Martingale usually does not continue increasing position size after losses, so its tail-loss structure is different. However, it depends on trend continuation. If positions are added after profits and then the trend reverses, it may also generate a large drawdown.